Vladimir Putin just sparked what could end up being one of the ugliest oil price wars in modern history, and American oil and gas companies may be the victims.

This weekend Saudi Arabia dropped the oil bomb. It not only cut its forward crude price to Chinese customers by as much as $6 or $7 per barrel, but is also reportedly looking to raise its daily crude output by as many as 2 million barrels per day into an already oversupplied global market. Look out below.

The move by the Saudis is both a market share grab and a loud signal to Moscow that it's done playing games. The dramatic action is in response to a contentious, and ultimately failed, OPEC meeting in Austria on Friday. OPEC members laid out a proposal to further cut oil output quotas by as much as 1.5 million barrels per day.

OPEC itself was aligned on the deal, but non-OPEC member Russia said "nyet," effectively killing it. A source inside the negotiations tells me that as the two sides worked out production cut plans, in the end the "red lines weren't even close." The source added that the Russians "definitely don't want to continue to support shale" at least in part because the Rosneft sanctions were still "too raw."

It was only three weeks ago that the Trump administration imposed sanctions on Russian oil giant Rosneft for transporting Venezuelan oil. Secretary of State Mike Pompeo believes that in helping Venezuela sell oil, Russia is effectively propping up the Maduro regime. Rosneft is run by Igor Sechin, a former employee and close friend of Putin.

Connect the dots. Putin reacting to Trump. The Saudis, led by Energy Minister and son of the king Abdulaziz bin Salman, reacting to Putin. And American oil and gas workers and investors are caught in the middle of this epic ego battle.

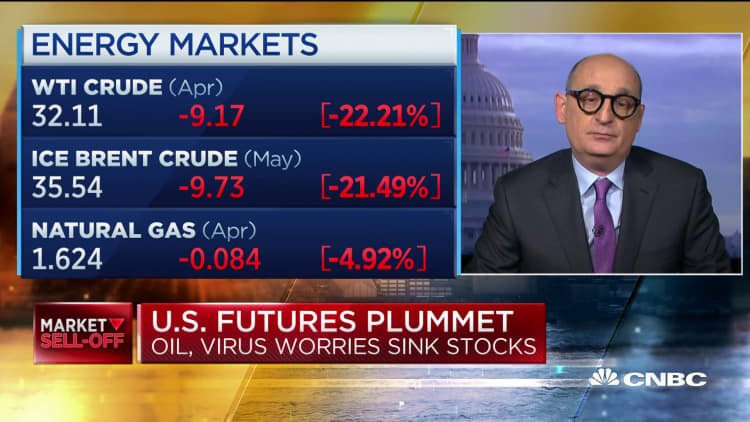

It couldn't occur at a worse time. Coronavirus is already slamming global oil demand and crude prices have fallen 30% this year. Italy is trying to severely limit population movement in its most important economic region for a month, one which is responsible for about 20% of the nation's economy. Put another way: economically, Italy is trying to lock down the output of California, Oregon and Washington states combined. For a month.

Could that happen here in the states? Unlikely, but there is a real risk of a sharp economic hit, as travel slows and people are asked to work from home. As the world's biggest consumer, we use about 20 million barrels of oil per day. So even a small slowdown would have a huge impact on global supply and demand.

Many industry people I spoke with over the weekend expect oil to open trading in the $30 dollar range, if not worse by week's end. That's very bad news for Texas, North Dakota and anyone still left invested in oil and gas stocks. Shares of Chevron are down 20% in 2020, making it the best performing energy stock in America. Most are down 30%, 40% or even 50% since January 1st. The S&P Oil & Gas ETF (XOP) is down 33% this month.

The industry is facing a three-sided attack: falling prices, a move of institutional investors to divest from fossil fuel companies, and crushing debt loads.

Debt is the problem. The U.S. oil and gas industry has about $86 billion of rated debt due in the next four years, according to Moody's. Nearly all of that debt is either junk rated, or rated just above junk. Fifty-seven percent of that is due in just the next two years. As oil prices fall and credit markets tighten, many companies won't be able to refinance their debts or extend maturities.

Time is the only friend many companies now have. Most energy debt isn't due until 2022, so some producers may be able to hang on, hoping for a turn. But if a turn doesn't come, it will be brutal. Energy executive Dan Pickering tweeted out Friday, "Maturities are a bit further out .. 2021/2022 will be Armageddon if current environment holds through 2020."

It's a greater risk than just oil. While energy stocks make up a paltry 4.4% of the S&P 500 weighting, energy related debt is 11% of the popular junk bond ETFs HYG and JNK. It makes up a big portion of corporate debt, which matters to banks both large and regional. The energy debt web is complicated and it is costly.

What everyone I've spoken with over the weekend agrees on is that industry leaders have to react swiftly and strongly, cutting costs and output immediately.

An energy executive, who didn't wish to be named, told me by phone Sunday that in his view, every industry CEO needs to come out tomorrow and say that they are shutting down all new drilling activity, cutting CapEx, slicing dividends and aggressively trying to reduce output.

It sounds extreme, but his point was that unless U.S. production comes down by a few million barrels per day, fast, oil could easily fall into the $20s, which would crush the value of in-ground reserves that serve as the basis for so much debt collateral in the industry. Banks will realize it no longer makes sense to operate a business with hugely negative cash flow.

More simply put, if we fall to $25-$30 per barrel for an extended period of time, many traders and executives I've spoken with in the past 24 hours believe that stockholder pain will only get worse, and bankruptcy lawyers will be busy.

Everyone seems to have a different opinion of how this ultimately plays out. Perhaps Russia comes back to the table, spooked by the Saudi move, and prices stabilize when an output cut deal is made. Or maybe oil prices crash and many U.S. equities trade even further down.

What everyone does seem to agree on is that the shale industry, its employees and its remaining investors are going to experience very sharp pain in the near term. A Capital IQ search shows that publicly traded oil and gas companies employ nearly 700,000 people. That's not including the millions more who work for private companies or in the halo of the industry.

The larger risk is that this pain seeps into the broader U.S. credit markets, all at a time when the coronavirus is starting to impact the economy as well. If a few million Americans stop traveling and commuting and work from home instead, gasoline demand will plummet, putting further pressure on prices.

As gas prices fall, you will no doubt hear the "lower gas prices will rescue the consumer" angle. While there is a benefit to Americans saving on gasoline, it's unlikely any amount of additional consumer savings will mitigate the damage of an entire industry facing mass layoffs and huge capital spending cuts.

It's not media hyperbole to call what happened this weekend in the oil markets "historic." When the Russians walked out of OPEC's Austria headquarters, it suddenly became every country – and every U.S company – for itself. A race to the top in production and a race to the bottom in prices.

Somewhere Vladimir Putin is looking at a map of Texas and smiling.

Subscribe to CNBC PRO for exclusive insights and analysis, and live business day programming from around the world.